How the Seller Disclosure Law of PA Affects Buyers and Sellers

-

July 2026

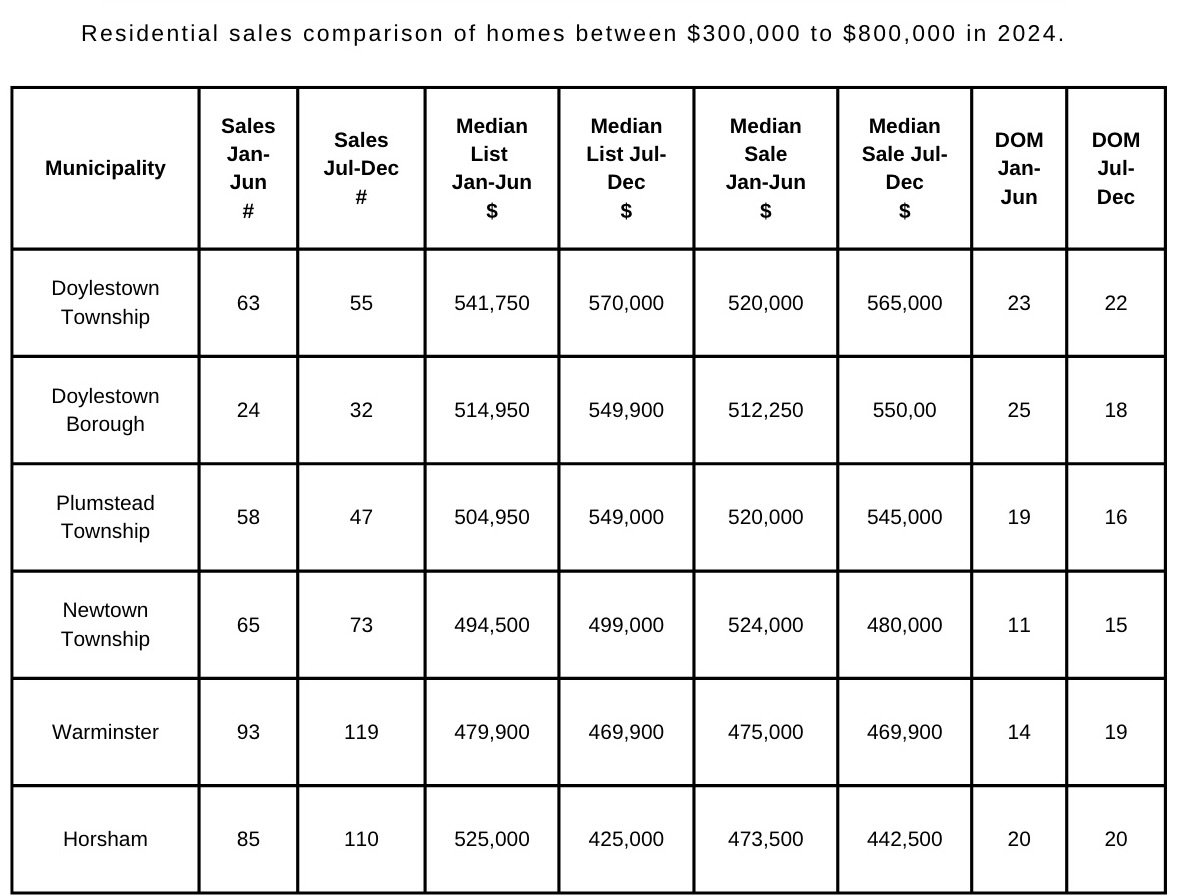

- Jul 20, 2026 Real Estate Market Updates: July 2026 Jul 20, 2026

-

April 2026

- Apr 1, 2026 Book of the Month: The Untethered Soul by Michael A. Singer Apr 1, 2026

-

February 2026

- Feb 21, 2026 Book of the Month: The 4 Disciplines of Execution by Chris McChesney, Sean Covey, and Jim Huling Feb 21, 2026

- Feb 9, 2026 How the Seller Disclosure Law of PA Affects Buyers and Sellers Feb 9, 2026

-

January 2026

- Jan 19, 2026 What To Expect In Real Estate Trends For 2026 Jan 19, 2026

- Jan 11, 2026 Book of the Month: Deep Work by Cal Newport Jan 11, 2026

- Jan 4, 2026 Your One Action for 2026 Jan 4, 2026

-

December 2025

- Dec 31, 2025 Top Stories of the Year Dec 31, 2025

- Dec 19, 2025 Book of the Month: Mastery by Robert Greene Dec 19, 2025

- Dec 15, 2025 Removing Popcorn Ceilings For a Cleaner Finish Dec 15, 2025

- Dec 7, 2025 Late Fall Real Estate Market Updates Dec 7, 2025

-

November 2025

- Nov 23, 2025 Book of the Month: Peak: Secrets From the New Science of Expertise by Anders Ericsson and Robert Pool Nov 23, 2025

- Nov 19, 2025 8 Home Maintenance Tasks To Check Off Your List Before Winter Nov 19, 2025

-

October 2025

- Oct 23, 2025 Book of the Month: Find Your Why by Simon Sinek Oct 23, 2025

- Oct 13, 2025 How Capital Gains May Impact Real Estate Decisions Oct 13, 2025

- Oct 2, 2025 Me Meetings to Get Priority Tasks in Order Oct 2, 2025

-

September 2025

- Sep 25, 2025 5 Soccer Teambuilders Any Coach Can Use Right Now Sep 25, 2025

- Sep 17, 2025 What to Know about a Home Appraisal Contingency Sep 17, 2025

- Sep 11, 2025 Teambuilding to Start the Season on the Same Foot Sep 11, 2025

- Sep 5, 2025 Book of the Month: The 5 Types of Wealth by Sahil Bloom Sep 5, 2025

-

August 2025

- Aug 28, 2025 Rent vs Buy: By the Numbers Aug 28, 2025

- Aug 22, 2025 Leaving Everything on the Field Aug 22, 2025

- Aug 17, 2025 Books of the Month: The Creative Act: A Way of Being by Rick Rubin and The War of Art by Steven Pressfield Aug 17, 2025

- Aug 13, 2025 Rent vs Buy: How to Choose Aug 13, 2025

- Aug 6, 2025 Inspection Contingencies and Timelines Aug 6, 2025

- Aug 3, 2025 Lessons From Painting and Soccer Camp Aug 3, 2025

-

July 2025

- Jul 23, 2025 Finding the Point Jul 23, 2025

- Jul 16, 2025 Book of the Month: Think Like a Monk: Train Your Mind for Peace and Purpose Every Day by Jay Shetty Jul 16, 2025

- Jul 9, 2025 Real Estate Market Updates: June 2025 Jul 9, 2025

- Jul 2, 2025 Taking Time Out to Re-Align Jul 2, 2025

-

June 2025

- Jun 25, 2025 Navigating Home Sale Contingencies Jun 25, 2025

- Jun 17, 2025 The Crossing Fawn Jun 17, 2025

- Jun 4, 2025 Book of the Month: Notes from a Deserter by C.W. Towarnicki Jun 4, 2025

-

May 2025

- May 29, 2025 We Are What We Eat May 29, 2025

- May 22, 2025 The Ins and Outs of Mortgage Contingencies May 22, 2025

- May 8, 2025 Coaching Fundamentals: Reflect and Repeat May 8, 2025

-

April 2025

- Apr 23, 2025 How Rory McIlroy Remained Present to Win the Masters Apr 23, 2025

- Apr 2, 2025 Coaching Fundamentals: Mastering the Demonstration for Player Understanding Apr 2, 2025

-

March 2025

- Mar 12, 2025 Book of the Month: Atomic Habits by James Clear Mar 12, 2025

-

February 2025

- Feb 27, 2025 5 Answers For Potential Homebuyers Entering the Spring Market Feb 27, 2025

- Feb 6, 2025 Investing Basics with Chris Strivieri, Founder and Senior Partner of Intuitive Planning Group in Alliance with Equitable Advisors Feb 6, 2025

-

January 2025

- Jan 30, 2025 Book of the Month: The MetaShred Diet Jan 30, 2025

- Jan 20, 2025 Residential Housing Trends in 2025 Jan 20, 2025

- Jan 9, 2025 Understanding the Use and Occupancy Certificate Jan 9, 2025

-

December 2024

- Dec 4, 2024 Book of the Month: How Champions Think by Dr. Bob Rotella Dec 4, 2024

-

November 2024

- Nov 19, 2024 Professional Spotlight: Fran Weiss, Owner of Weiss Landscaping Nov 19, 2024

-

October 2024

- Oct 29, 2024 Book of the Month: Hidden Potential by Adam Grant Oct 29, 2024

- Oct 21, 2024 Professional Spotlight: James George, President, Global Mortgage Oct 21, 2024

- Oct 15, 2024 Buyers Post-NAR Settlement Oct 15, 2024

Whether listing your home or purchasing a home in Pennsylvania, a Seller’s Disclosure is one of the most important documents in a real estate transaction. The Seller’s Disclosure is a form used by a seller to provide information about the condition of the property or known material defects in and around a property prior to a sale.

Prior to 2000, buyers in Pennsylvania were in a position of caveat emptor, or buyer’s beware. It was the responsibility of the buyer to perform their due diligence about the condition of a potential property and uncover any of the wide number of issues that may impact the functionality and safety. The addition of the Seller Disclosure Law is one of many ways in which a consumer of real estate has gained more transparency about a potential purchase.

The Seller Disclosure Law applies to any interest in the transfer of real estate that contains between one and four residential dwellings. Though a buyer is purchasing a property “as is,” with terms that can be negotiated between parties, the seller has an obligation to inform a buyer on the property’s known condition. A seller must provide a seller’s disclosure form prior to a transaction and cannot provide false or misleading information about the property, including known material defects.

Some of the areas of a property subjected to the seller’s disclosure include the roof, attic, basement/crawl space, any additions or alterations, plumbing, HVAC, water and sewer, hazardous materials, windows, water intrusions, and the appliances or fixtures included in the Agreement of Sale, among others.

There are a few exceptions in which a seller does not need to complete a Seller’s Disclosure form.

If the property is being sold through administration, guardianship, conservatorship, or through a trust, the seller’s disclosure is not required, but the noted executor is required to disclose any known defects. If the property is a new construction transfer, the property does not require a seller’s disclosure if the builder issues a home warranty good for one year or longer and the property has been inspected and determined to be up to code according to the local township.

A commercial property that includes four or less dwellings (ex. storefront w/ upstairs units or a farm w/ additional units to rent) is responsible for a seller’s disclosure, however, a multi-unit property with more than four units does not require a seller’s disclosure because multi-unit properties are subjected to use and occupancy certificates prior to a transfer, which require an inspection and specific items in the dwelling to be up to code according to the local municipality.

Condo and coop owners are required to share a seller’s disclosure, but only for their specific unit and not the common areas.

Other exceptions include the transfer from one co-owner to another, a transfer to a spouse or direct descendent, the transfer of a property about to be demolished, or the transfer of a property that is court-ordered either through a foreclosure process or divorce settlement from one spouse to the other.

Even if the seller never lived in the property (i.e. a landlord), the seller still has in-depth knowledge of the property and must complete the SD. A power of attorney must complete the SD, however, they are only required to provide relevant information to the best of their ability.

Depending on the state of the probate process, a seller’s disclosure is not required if the property is being sold by the estate so the proceeds can be distributed to the beneficiaries. However, if the beneficiaries have inherited the property and taken title, they are required to provide a SD.

It’s also important to note that anything that is not material (i.e. previous injuries, deaths, ghosts, mental anguish) does not need to be disclosed.

If a seller is found to be aware of a problem they did not disclose, they may be responsible for any financial losses or repairs incurred by the buyer. Proving the seller withheld information or knowingly covered up defects is sometimes difficult to prove, so contacting a real estate attorney is the first step for a buyer if they uncover an issue that should have been disclosed. Litigation must be presented within two years of settlement.

For an example of how the law has been applied in Pennsylvania, read more here:

For more information on the PA Seller Disclosure Law: